How to Add an Inventory Item in QuickBooks

by Laura Madeira | July 1, 2013 9:00 am

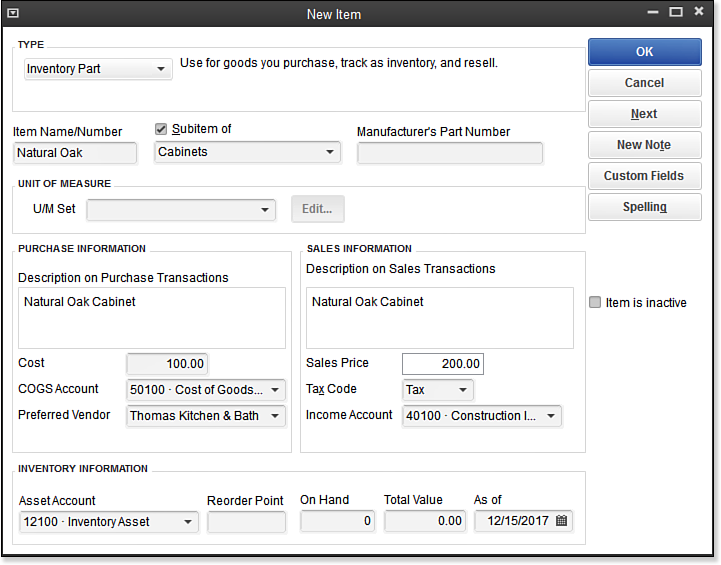

When you purchase or build a product, and stock it in your warehouse for future sale to your customer, you should create an inventory part, as shown here:

[1]

[1]Adding a new inventory part item.

When inventory is used, an Inventory Asset account is increased when you purchase and stock the product. The income and related cost is not recorded until you include the inventory item on your customer’s invoice.

To practice adding a new inventory part item, open the sample data file, as instructed in Chapter 1 of Laura Madeira’s QuickBooks 2013 In Depth[2] titled “Getting Started with QuickBooks:”

- On the Home page, click the Items & Services icon. The Item List displays.

- Click the Item button in the lower-left corner, and select New or use the keyboard shortcut of Ctrl+N. The New Item dialog box displays.

- In the Type drop-down list, select Inventory Part.

- In the Item Name/Number field, type Natural Oak Cabinet.

- Check the Subitem Of checkbox and then select Cabinets from the drop-down list.

- Leave the boxes for Manufacturer’s Part Number and U/M Set (for Unit of Measurement) blank.

- In the Description on Purchase Transactions box, select the newly created Natural Oak Cabinet.

- In the Cost field, type 100.00.

- From the Account drop-down list, select the Cost of Goods Sold account, if it isn’t automatically selected by QuickBooks.

- In the Preferred Vendor field, select or begin typing Thomas Kitchen & Bath , and the existing vendor name populates the field.

- In the Sales Price field, type 200.00.

- Leave the default of Tax assigned in the Tax Code field.

- In the Income Account drop-down list, select the Construction Income:Materials Income account. You can also select the account by typing 40100 (the account number) in this example.

- In the Asset Account drop-down list, leave the Inventory Asset account that displays by default. (Optional) Enter a quantity for Reorder Point reporting.

- Leave the On Hand field blank. See the Caution that follows about entering your quantity on hand in this manner. If you choose to enter an On Hand quantity, QuickBooks enters a financial transaction that increases the inventory asset account and increases the Opening Balance Equity account.

- If you entered an On Hand quantity (not recommended), QuickBooks automatically calculates the Total Value field by taking the On Hand quantity times the amount recorded in the Cost field. You can override this calculated Total Amount field, but you should do so only if the resulting value is the proper amount to record for this asset. (See the Caution that follows.)

- If you entered an On Hand quantity, select the As Of date you want to record the increase in your inventory asset value.

- Click OK to save your changes and close the New Item dialog box.

–> A word of caution: Converting to QuickBooks after having used other software to track inventory? It is recommended you use an Inventory Adjustment transaction to enter your opening quantity on hand instead of entering a quantity in the On Hand field of a new inventory item record. For more information, see “Adjusting Inventory,” p. 195 of Laura Madeira’s QuickBooks 2013 In Depth[2].

Offering a new product for sale to your customers? You should not enter an amount in the On Hand field; instead use a Create Purchase Orders, Enter Bills, or Write Checks transaction to record the purchase of this new inventory item.

After you save a new item record, many fields cannot be edited, including the On Hand and Total Value fields.

The following are optional fields or actions in an item record (depending on the version of QuickBooks you are using) that are useful:

- U/M Set—Used to assign default units of measure for purchases, sales, and shipping of the selected item.

- Notes—Internal notes for the currently selected item.

- Custom Fields—Flexibility to add information that is not already tracked by QuickBooks. Review the section in Chapter 5 of Laura Madeira’s QuickBooks 2013 In Depth[2] titled “Inventory Features by QuickBooks Edition” to see if the custom field you need is already tracked in a different edition of QuickBooks, than the edition you are currently using.

- Spelling—Click Spelling, and QuickBooks will spell check the description fields of the individual item being added or edited.

- Item Is Inactive—Should be used only when the item inventory count for the selected item is zero, and when you no longer want the item to be included in drop-down lists. More information on efficiently managing your items is included in Chapter 4 of Laura Madeira’s QuickBooks 2013 In Depth, in the section titled “Making an Item Inactive.”

Here’s another tip from Laura Madeira’s QuickBooks 2013 In Depth:

The Cost field in a new (or edit) inventory part record is optional. Entering a default cost can be useful for automating entry on purchase transactions, and in some instances can help with properly reporting a change in value when an inventory adjustment record is recorded.

From Laura Madeira’s QuickBooks 2013 In Depth[2]

- [Image]: http://www.quick-training.com/wp-content/uploads/2013/05/5.6.bmp

- QuickBooks 2013 In Depth: http://www.quick-training.com/quickbooks-2013-in-depth/

Source URL: http://www.quick-training.info/2013/07/01/how-to-add-an-inventory-item-in-quickbooks/